Are you struggling with debt and looking for a way to negotiate with your creditors? A sample letter to creditors to settle debt can help you communicate your intentions clearly and effectively.

In this article, we will provide you with templates, examples, and samples of letters that you can use to reach out to your creditors and work towards a settlement agreement.

With our easy-to-use resources, you can take the first step towards resolving your financial issues and finding a path towards a debt-free future.

Sample Letter to Creditors to Settle Debt

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Creditor Name]

[Creditor Address]

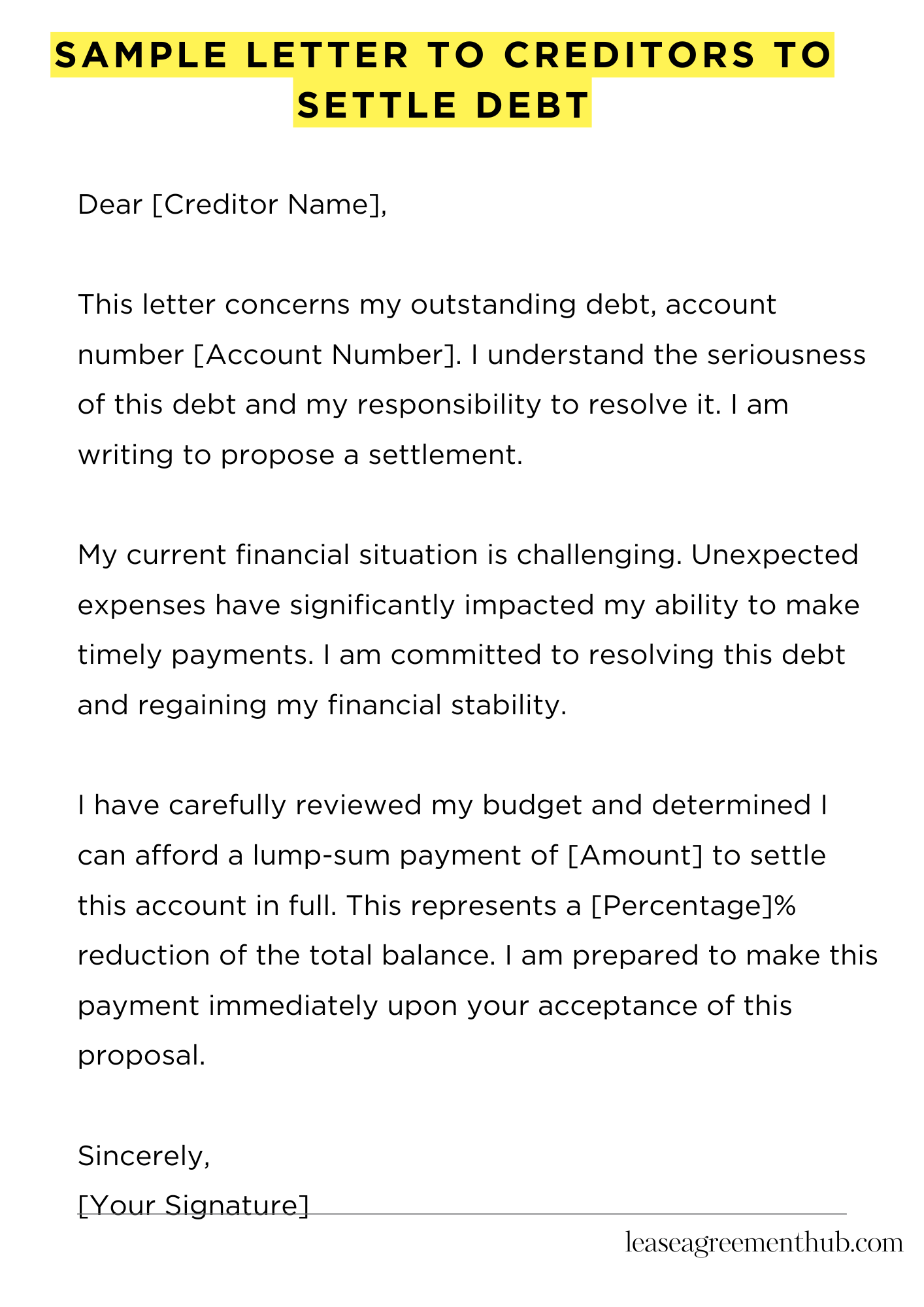

Dear [Creditor Name],

This letter concerns my outstanding debt, account number [Account Number]. I understand the seriousness of this debt and my responsibility to resolve it. I am writing to propose a settlement.

My current financial situation is challenging. Unexpected expenses have significantly impacted my ability to make timely payments. I am committed to resolving this debt and regaining my financial stability.

I have carefully reviewed my budget and determined I can afford a lump-sum payment of [Amount] to settle this account in full. This represents a [Percentage]% reduction of the total balance. I am prepared to make this payment immediately upon your acceptance of this proposal.

I understand this offer may not fully cover the outstanding debt. However, I believe it represents a fair and reasonable solution given my current circumstances. I am confident this settlement will be more beneficial than pursuing lengthy and costly collection efforts.

Please consider my proposal. I look forward to your prompt response and am available to discuss this matter further. Thank you for your time and consideration.

Sincerely,

[Your Signature]

How to Write a Sample Letter to Creditors to Settle Debt

Understanding the Nuances of Debt Settlement

Negotiating debt settlement requires a nuanced approach. It’s not simply a matter of asking for a lower amount. You must present a compelling case, demonstrating your financial hardship and your genuine desire to resolve the outstanding balance. Successfully navigating this process necessitates meticulous planning and a clear understanding of your creditor’s perspective.

Gathering Essential Information: A Crucial First Step

Before composing your letter, diligently collect all relevant information. This includes the creditor’s name and address, your account number, the total debt amount, and any previous payment history. Accurate data forms the bedrock of a persuasive argument. Failure to include these details can significantly weaken your position.

Crafting a Persuasive Narrative: The Art of the Plea

Your letter should articulate your financial predicament with candor and empathy. Avoid obfuscation; clearly explain the reasons for your inability to meet your payment obligations. Highlight extenuating circumstances, such as job loss or unforeseen medical expenses, while maintaining a tone of responsibility and remorse. This is where you show, you are not simply trying to shirk your responsibility.

Proposing a Concrete Settlement Offer: A Tangible Solution

Offer a specific, realistic settlement amount. This should be a lump-sum payment you can realistically afford. Research suggests a settlement offer between 50-60% of the total debt is often a reasonable starting point. However, your individual circumstances will dictate the appropriate proposal.

Structuring Your Letter for Maximum Impact: A Formal Approach

Maintain a formal and professional tone throughout the letter. Use concise language, avoiding jargon or overly emotional pleas. Organize your points logically, presenting your case step-by-step. A well-structured letter displays respect while enhancing the credibility of your proposal. Use a business letter format.

The Importance of Maintaining Documentation: A Paper Trail

Retain copies of all correspondence, including your initial letter, any subsequent communications, and any agreed-upon settlement documents. This documentation will serve as crucial evidence should any disputes arise. Methodical record-keeping is paramount in debt resolution.

Following Up After Dispatch: Persistence Pays Off

After sending your letter, allow a reasonable time for a response. If you don’t hear back within a specified timeframe (two to three weeks is a good guideline), follow up with a phone call or a polite, concise email. Remember, persistence often proves key in achieving a favorable resolution. Don’t be dissuaded by initial silence – some creditors need time to assess your proposal. Act professionally.

FAQs about sample letter to creditors to settle debt

What information should I include in a debt settlement letter?

Your letter should clearly state the debt you’re addressing, the creditor’s name and account number, the outstanding balance, and your proposed settlement amount. Include your contact information and a timeframe for your response. Consider including documentation like a copy of your most recent statement.

How much should I offer to settle my debt?

The amount you offer will depend on several factors, including your current financial situation, the age of the debt, and the creditor’s typical settlement practices. Researching average settlement rates for similar debts can be helpful, but be prepared to negotiate.

What if the creditor rejects my initial offer?

Be prepared for the possibility of rejection. Have a counter-offer ready, or be willing to negotiate further. Clearly articulate your reasons for your offer, highlighting your financial constraints and willingness to resolve the debt.

Should I get legal advice before sending a debt settlement letter?

Seeking legal counsel is advisable, especially if dealing with complex debts or multiple creditors. An attorney can help you understand your rights and ensure your letter is legally sound and protects your interests.

What happens after I send the letter?

After sending your letter, wait for the creditor’s response. They may accept your offer, counter-offer, or reject it outright. Keep detailed records of all communication, including dates, times, and the content of conversations or correspondence.

Related: