Facing debt? A letter to your creditors explaining your inability to pay is crucial. It shows you’re taking responsibility and trying to work things out.

This article provides sample letters. These are templates. They’re designed to help you craft your own message. We’ll give you different examples.

Use these samples as a starting point. Adapt them to your unique situation. This will help you communicate effectively with your creditors.

sample letter to creditors unable to pay

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Creditor Name]

[Creditor Address]

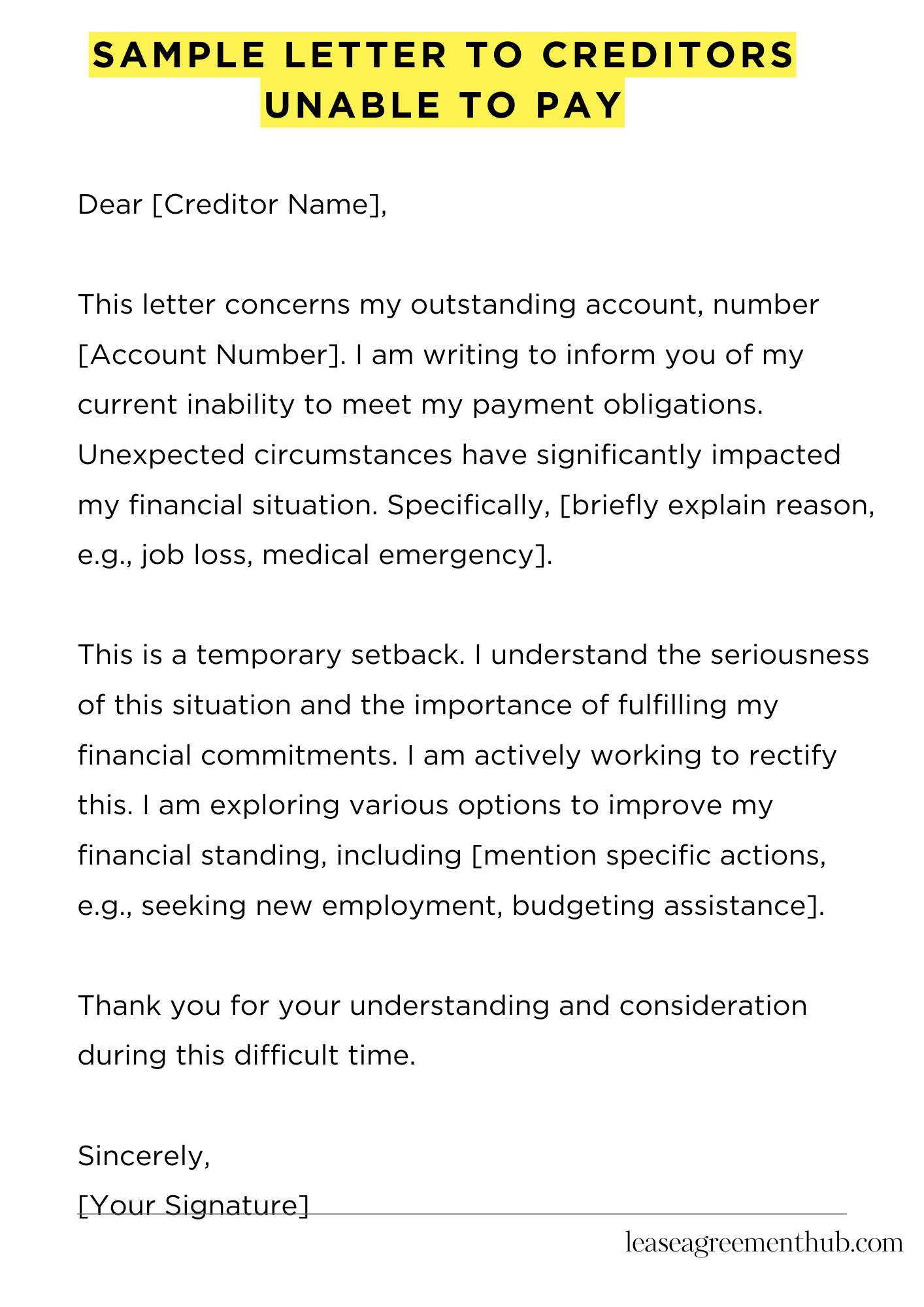

Dear [Creditor Name],

This letter concerns my outstanding account, number [Account Number]. I am writing to inform you of my current inability to meet my payment obligations. Unexpected circumstances have significantly impacted my financial situation. Specifically, [briefly explain reason, e.g., job loss, medical emergency].

This is a temporary setback. I understand the seriousness of this situation and the importance of fulfilling my financial commitments. I am actively working to rectify this. I am exploring various options to improve my financial standing, including [mention specific actions, e.g., seeking new employment, budgeting assistance].

I would greatly appreciate the opportunity to discuss a payment plan that works for both of us. I am available to speak at your earliest convenience. Please contact me to arrange a time to discuss this further. I am committed to resolving this debt as quickly as possible.

Thank you for your understanding and consideration during this difficult time.

Sincerely,

[Your Signature]

How to Write a Sample Letter to Creditors Unable to Pay

Understanding the Gravity of the Situation

Facing insurmountable debt can be profoundly disheartening. Procrastination is a deleterious habit in such circumstances. Ignoring creditors only exacerbates the problem, potentially leading to dire legal ramifications. A proactive approach, embodied in a well-crafted letter, is crucial. This communication serves as a bridge, initiating a dialogue towards a mutually agreeable resolution.

Crafting Your Salutation: A Necessary Precursor

Begin with a formal salutation, addressing the creditor by name and title if known. Generic greetings lack the gravitas needed in such a delicate matter. Precision is paramount. Avoid informality; maintain a professional tone throughout your correspondence. This initial step sets the stage for a constructive conversation.

Articulating Your Predicament: Honesty is the Best Policy

Clearly and concisely explain your current financial predicament. Avoid euphemisms; state the facts directly. Detail the reasons for your inability to meet your obligations. Transparency is key to building credibility and fostering empathy. Cite specific events or circumstances impacting your income. Be succinct but exhaustive.

Proposing a Plan: A Roadmap to Resolution

Don’t simply state your inability to pay; propose a concrete plan. This could involve a partial payment, a renegotiated payment schedule, or a debt consolidation strategy. Demonstrate your commitment to resolving the debt. Detail your proposed timeline and repayment terms with meticulous accuracy. Provide concrete examples, showing your commitment.

Gathering Necessary Documentation: Supporting Your Claims

Prepare supporting documentation to substantiate your claims. This might include pay stubs, bank statements, or medical bills. Providing irrefutable evidence lends weight to your assertions, boosting your credibility and strengthening your negotiating position. This meticulousness demonstrates your seriousness.

Maintaining a Professional Tone: A Delicate Balancing Act

While expressing your financial hardship, maintain a professional and respectful tone. Avoid making excuses or accusations. Focus on finding a solution that works for both parties. Remember: civility is your strongest ally in this negotiation. A conciliatory approach is far more effective than antagonism.

Review and Send: Completing the Process

Before sending your letter, meticulously review it for any errors or omissions. Ensure clarity and conciseness. Proofreading is paramount. Send your letter via certified mail with return receipt requested, providing irrefutable proof of delivery. This final step ensures accountability and transparency.

FAQs about sample letter to creditors unable to pay

Communicating with creditors when facing financial hardship can be challenging. A well-crafted letter can significantly improve the outcome of the situation.

What information should I include in a letter to creditors explaining my inability to pay?

Your letter should clearly state your inability to make payments, provide a brief and honest explanation for your financial difficulties (without excessive detail), and propose a plan of action. This plan might include a request for a payment plan, a reduced payment amount, or an explanation of when you anticipate being able to resume full payments. Include your account numbers and relevant contact information.

Should I admit to my debt and the amount owed in the letter?

Yes, it’s crucial to be transparent and acknowledge the debt and the outstanding amount. Denying the debt will likely damage your credibility and hinder any potential for a positive resolution. Accuracy is vital here to avoid further complications.

What tone should I adopt in my letter to creditors?

Maintain a respectful, professional, and apologetic tone. Avoid being confrontational or making excuses. A sincere and concise explanation of your situation, coupled with a proactive approach to finding a solution, is more likely to elicit a positive response from the creditor.

Is it necessary to send a letter by certified mail?

While not always mandatory, sending your letter via certified mail with return receipt requested provides proof of delivery. This is highly recommended for establishing a record of your communication with the creditor, particularly if you anticipate potential disputes.

What should I do if the creditor does not respond to my letter?

If you don’t receive a response within a reasonable timeframe (typically 2-3 weeks), follow up with a phone call. If the phone call is also unproductive, consider seeking advice from a credit counselor or debt management professional. They can offer guidance on further steps to take.

Related: